Hawala is the main means by which migrants move money, a system that enables users to transfer cash via an ancient compact founded solely on trust. It’s use has expanded with the millions of MidEast migrants moving towards the EU since the start of the Syrian conflict.

It’s banking at it’s simplest, devised by medieval tradesmen who needed to outsmart highway robbers on the dangerous Silk and Spice Roads. The same benefits apply today to migrants crossing international borders. While it could serve criminal activity, experts maintain that’s a tiny fraction of all hawala transactions.

As in antiquity, it operates off-the-books and under-the-radar of governments, tax collectors, and institutional banks. It’s not totally unlike today’s peer-to-peer transactions using digital currency like Bitcoin or Litecoin, which some believe will soon be used in halawa. When it comes to commerce, cutting out the middle man never gets old.

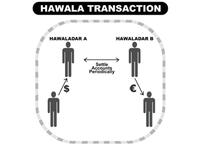

in one city to be transferred to a recipient in another location. They agree a password that will permit the end payout. Hawaladar #1 calls hawaladar #2 in the recipient's city, informs #2 as to the password, and relays any other instructions for releasing funds.")

use hawala. It moves billions more to developing nations as workers send wages home. Hawala is maximally flexible in that sums can be redeemed in multiple currencies, paid in-full on-demand or as per client-defined pay-out stages.")

in one city to be transferred to a recipient in another location. They agree a password that will permit the end payout. Hawaladar #1 calls hawaladar #2 in the recipient's city, informs #2 as to the password, and relays any other instructions for releasing funds.")

use hawala. It moves billions more to developing nations as workers send wages home. Hawala is maximally flexible in that sums can be redeemed in multiple currencies, paid in-full on-demand or as per client-defined pay-out stages.")